- ■

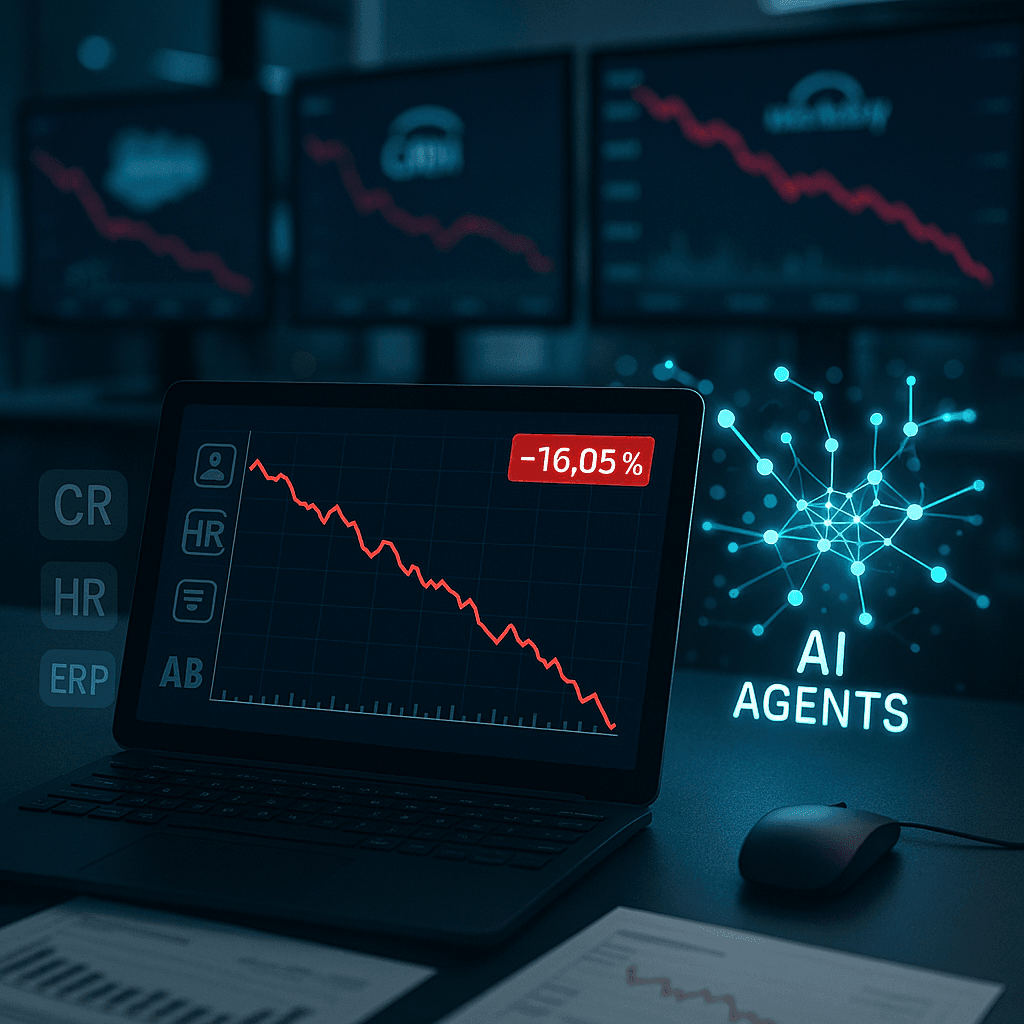

ServiceNow plummeted over 16% following earnings results, marking one of the steepest single-day drops for the enterprise software giant

- ■

The selloff triggered sector-wide contagion, pulling down Salesforce, Workday, and Oracle as AI disruption fears escalate

- ■

IBM results compounded concerns about traditional software vendors’ ability to compete in the AI era

- ■

Investors are rotating out of legacy SaaS names amid questions about pricing power and competitive moats against AI-native solutions

The enterprise software sector just hit a wall. ServiceNow shares cratered more than 16% in Thursday trading, triggering a brutal selloff across the entire software landscape as investors flee on mounting fears that AI is fundamentally disrupting traditional SaaS business models. The carnage spread fast – Salesforce, Workday, and Oracle all tumbled in sympathy, while IBM results added fuel to the fire.

ServiceNow just delivered a wake-up call that’s rattling the entire enterprise software establishment. The IT service management giant’s shares nosedived more than 16% on Thursday, erasing billions in market value and sending shockwaves through a sector that’s spent months trying to convince Wall Street it can thrive in the AI era.

The timing couldn’t be worse. Just as legacy software vendors were gaining confidence that they could successfully pivot to AI-powered offerings, the market delivered a brutal reality check. ServiceNow‘s collapse didn’t stay contained – it metastasized across the software landscape like a virus. Salesforce shares tumbled, Workday got hammered, and Oracle couldn’t escape the bloodbath.

What’s driving the panic isn’t just one company’s numbers. It’s a fundamental reckoning about whether traditional SaaS business models can survive when OpenAI, Microsoft, and Google are offering AI agents that can automate the exact workflows these companies charge premium subscriptions to manage. The existential question hanging over the sector: why pay $100 per user per month for enterprise software when an AI agent can do the same work for pennies?

IBM‘s results only deepened the gloom. The Big Blue’s numbers revealed the pressure legacy tech vendors face as customers delay software purchases while evaluating AI-native alternatives. It’s a pattern that’s emerging across earnings season – enterprises hitting pause on traditional software commitments as they wait to see how AI reshapes their technology stack.

The contagion reflects Wall Street’s growing conviction that the enterprise software playbook of the past decade is broken. High-margin subscription models, sticky customer relationships, and predictable revenue streams – the very characteristics that made SaaS stocks darlings of the growth investing crowd – suddenly look vulnerable when AI can replicate core functionality at a fraction of the cost.

Investors are wrestling with uncomfortable questions. Can Salesforce maintain its CRM dominance when AI agents can manage customer relationships without expensive seat licenses? Does Workday‘s HR platform justify premium pricing when Microsoft embeds comparable AI capabilities into Office 365? How does Oracle compete when cloud-native AI infrastructure providers offer faster, cheaper alternatives?

The selloff marks a sharp reversal from earlier optimism. Many of these companies had rallied on promises of AI integration, with executives touting how they’d embed large language models and generative AI features into existing products. But the market’s message today is clear: bolting AI onto legacy architecture isn’t enough. Investors want proof that traditional software vendors can defend margins and market share against purpose-built AI competitors.

What’s particularly unnerving for the bulls is the speed of the rotation. Software stocks have been reliable performers for years, anchored by recurring revenue and enterprise switching costs. The fact that a single earnings miss can trigger sector-wide capitulation suggests confidence is cracking. Fund managers who’ve long treated enterprise SaaS as a safe haven are suddenly questioning whether these are value traps in an AI-first world.

The broader implications extend beyond individual stock prices. This selloff could reshape how enterprises budget for technology, how venture capital flows into B2B software startups, and how the next generation of enterprise tools gets built. If the market’s right about AI disruption, we’re watching the beginning of a generational shift in business software – not just a temporary earnings blip.

Analysts are scrambling to reassess valuations and growth assumptions. The companies hit hardest today trade at premium multiples justified by assumptions about durable competitive advantages. But if AI erodes those moats faster than expected, current valuations look increasingly difficult to defend. The question isn’t whether these companies will survive – they will – but whether they can maintain the growth rates and margins that support their stock prices.

The software sector’s brutal Thursday marks more than just a bad earnings day – it’s a referendum on whether legacy SaaS can adapt fast enough to an AI-first world. ServiceNow‘s 16% plunge and the resulting contagion across Salesforce, Workday, and Oracle signal that investors are no longer willing to give traditional vendors the benefit of the doubt. The companies that survive this transition will need to prove they can do more than slap AI features onto existing products – they’ll need to fundamentally reinvent their value proposition for an era when intelligent automation threatens to commoditize the workflows they’ve monetized for decades. For now, the market’s betting that transformation won’t come easy.

Leave a Reply