- ■

Wall Street analysts are increasingly bullish on neocloud providers despite warning signs about their business models

- ■

McKinsey research flags fragile economics for neoclouds that emerged as stopgaps during the GPU shortage

- ■

These providers face higher risk profiles compared to established AI infrastructure plays from Amazon, Microsoft, and Google

- ■

The tension highlights a broader debate about which AI infrastructure bets will survive long-term

Wall Street is warming up to neocloud providers – the scrappy AI infrastructure companies that emerged during the GPU shortage – but a new warning from McKinsey suggests investors might be walking into a trap. These stopgap providers filled a critical void when Nvidia chips were impossible to get, but their economics look shakier than traditional cloud plays, raising questions about whether the current bullish sentiment is justified.

Wall Street is developing an appetite for risk. Analysts are piling into neocloud providers – the new generation of GPU-as-a-service companies that sprouted up during the great chip shortage – even as McKinsey drops a cautionary note that should make investors think twice.

The consulting giant’s latest research warns that neoclouds, despite their momentum, operate on fragile economic foundations that set them apart from more established AI infrastructure plays. It’s a sobering counterpoint to the growing enthusiasm from the investment community, which has watched these companies capture market share while Amazon, Microsoft, and Google struggled to meet surging demand for AI compute.

Neoclouds emerged out of necessity. When the AI boom hit in late 2022 and early 2023, enterprises desperate for GPU access turned to anyone who could deliver. Companies like CoreWeave, Lambda Labs, and others rushed to fill the void, signing massive deals to secure Nvidia H100 chips and lease them to AI startups and enterprises at premium rates. The business model was simple: acquire GPUs, rent them out, profit.

But that simplicity masks underlying vulnerabilities that McKinsey’s analysis brings into focus. Unlike hyperscale cloud providers that benefit from diversified revenue streams, economies of scale, and vertically integrated infrastructure, neoclouds depend almost entirely on GPU arbitrage. They’re middlemen in a market where the terms can shift rapidly.

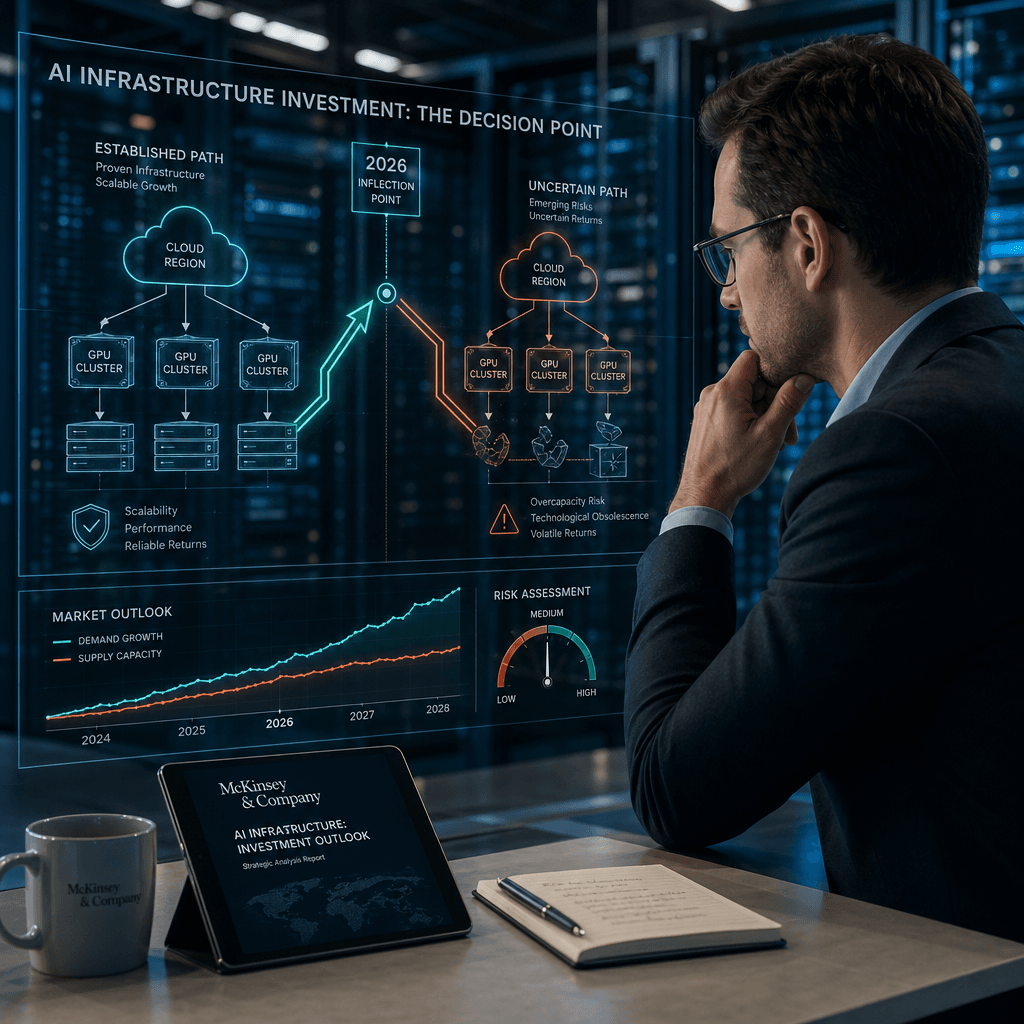

The economics get tricky when you dig into the details. Neoclouds typically lock in GPU supply through long-term purchase commitments, betting they can lease capacity at rates high enough to cover hardware costs, data center expenses, and generate profit. But GPU prices are notoriously volatile, and utilization rates can fluctuate. If demand softens or if the hyperscalers finally catch up on capacity, neoclouds could find themselves stuck with expensive hardware and nowhere to deploy it profitably.

There’s also the competitive angle. Amazon Web Services, Microsoft Azure, and Google Cloud aren’t sitting still. All three have announced massive infrastructure investments – Microsoft alone committed over $80 billion for fiscal 2025 – and they’re developing custom AI chips to reduce dependence on Nvidia. As that capacity comes online, the premium pricing that makes neocloud economics work could evaporate.

Yet Wall Street seems willing to overlook these risks, at least for now. The bullish case centers on continued AI infrastructure scarcity and the specialized services neoclouds provide. Unlike generic cloud compute, these providers offer optimized environments for training large language models, with networking configurations and software stacks purpose-built for AI workloads. That specialization commands a premium.

Some neoclouds are also pivoting to become more than just GPU rental shops. They’re building managed services, developing proprietary orchestration tools, and establishing partnerships with AI companies that could provide stickier revenue. CoreWeave’s reported pursuit of an IPO has only intensified investor interest in the category.

But McKinsey’s fragile economics warning cuts through the hype. The firm’s analysis suggests that without sustainable competitive advantages – whether through proprietary technology, exclusive partnerships, or operational efficiencies – neoclouds risk becoming commoditized infrastructure providers in a market dominated by giants with far deeper pockets.

The timing of this debate matters. We’re potentially approaching an inflection point in AI infrastructure. If the GPU shortage truly eases in 2026 as some analysts predict, and if hyperscalers successfully scale their custom chip alternatives, the window for neocloud dominance might be narrower than bulls expect. That makes these stocks inherently more volatile than betting on established cloud providers with diversified businesses.

For investors, the neocloud story presents a classic risk-reward tradeoff. There’s genuine upside if these companies can establish defensible positions before the market normalizes. But McKinsey’s warning serves as a reminder that not every AI infrastructure play is created equal, and the companies that thrived during a supply crunch might struggle when competition intensifies and margins compress.

The neocloud investment thesis comes down to timing and sustainability. Wall Street’s growing bullish stance reflects real opportunities in a market that’s still capacity-constrained, but McKinsey’s economics warning highlights the fragility lurking beneath the growth story. These aren’t the same as betting on AWS or Azure – they’re higher-risk plays that depend on market conditions staying favorable long enough for these companies to build moats. Investors drawn to the AI infrastructure boom need to distinguish between companies riding a temporary wave and those building businesses that can survive when the tide goes out. The next 12 to 18 months will likely determine which category neoclouds fall into.

Leave a Reply