- ■

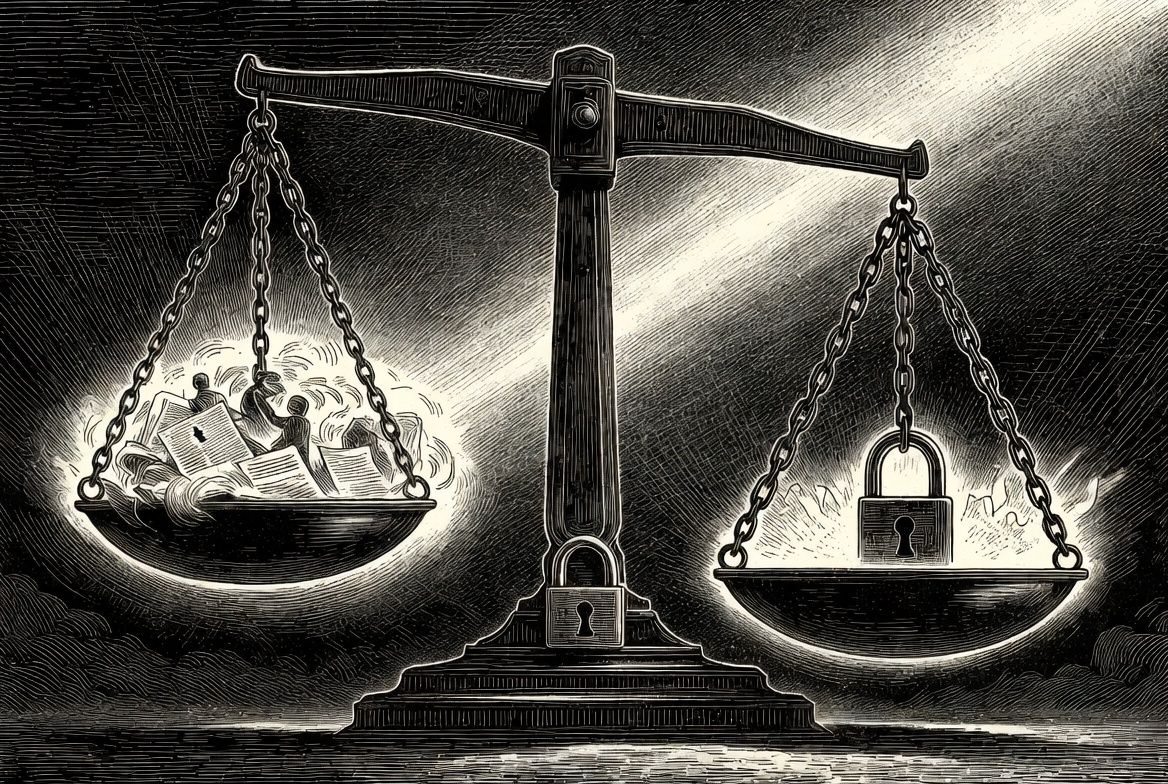

Prediction markets face a built-in tension: allowing insiders improves price accuracy because they hold the best signals, but restricting them improves fairness by preventing unequal informational advantage from shaping outcomes.

- ■

Even with enforcement mechanisms and identity systems, insider advantage persists because information spreads through informal networks and probabilistic behavior ensures leaks occur at the edges rather than being fully eliminated.

- ■

As markets scale across more events and participants, oversight cannot match the growth of informational pathways, leading to a persistent equilibrium where prediction markets remain partially informed, structurally asymmetric systems rather than fully fair or fully truth-maximizing ones.

At the heart of prediction markets sits a structural contradiction that can’t be legislated away or engineered out.

A market becomes more truthful as it absorbs better information. The highest-quality information, in many cases, is Material Nonpublic Information, the kind held by insiders close to decisions before they surface publicly.

A market becomes more fair as access to advantage is flattened. That requires restricting or eliminating the use of that same information.

So the system faces a permanent fork in the road. Let insiders trade and you get sharper prices with a moral hazard baked in. Lock them out and you preserve fairness at the cost of knowingly blinding the market to its best signals.

Regulators like the Commodity Futures Trading Commission openly wrestle with this tension. Their current posture is not about solving it, but about deciding where to sit on the spectrum.

Incentives: The Gravity You Can’t Escape

Strip away law and ethics, and the system reduces to incentives.

If someone holds valuable inside information, the payoff structure is brutally simple. Doing nothing yields zero. Acting discreetly offers a shot at significant gain. As long as detection is uncertain and punishment is probabilistic, some actors will move.

The case involving Gannon Ken Van Dyke illustrates the point with uncomfortable clarity. Even under military secrecy, with legal exposure and career risk, the expected reward was enough to trigger action.

That’s the deeper takeaway. Enforcement changes the frequency of violations, not their existence. The system always leaks at the edges because human behavior isn’t binary. It’s probabilistic.

Why Identity Systems Hit a Wall

KYC and surveillance feel like solid defenses until you follow the logic one step further.

Knowing who owns an account does not reveal who influences that account. A verified identity tells you the name on the door, not the conversations happening behind it.

Traditional markets rely on mapping insiders to trades. That works when the network is visible and contained. Prediction markets fracture that model:

- Participants are global.

- Events are diverse and constantly shifting.

- Relationships travel through private, informal channels.

Even highly regulated platforms can only detect patterns that look statistically unusual. They catch the loud signals. The quiet ones dissolve into the background.

The blind spot isn’t technical. It’s social. You can authenticate a person, but you cannot fully map their network.

The Hidden Web: Tippees and Distance

Financial law already acknowledges this with the concept of tippees. Information rarely stays with the original insider. It diffuses outward, moving through layers of distance and deniability.

In prediction markets, that diffusion accelerates. Information can pass through informal chains that cross borders, platforms, and identities before it surfaces as a trade.

Each step away from the source reduces traceability. By the time the signal hits the market, it may look indistinguishable from a well-informed guess.

That’s the structural invisibility problem. Not all advantages are observable, and the most dangerous ones often aren’t.

Scale: The System Outruns the Watchers

Even if you imagine perfect legal tools, you run into a simpler constraint: attention.

Markets multiply faster than oversight capacity. Each new contract introduces a new potential insider set, a new web of relationships, a new pattern to monitor.

Regulators tend to catch the extreme cases, especially when they intersect with national security or high-profile events. Those cases act as signals, reminders that enforcement exists.

But the majority of activity lives below that threshold. Not illegal enough to trigger alarms, not obvious enough to isolate, not large enough to prioritize.

The result is a persistent “dark matter” of undetected advantage.

The Nature of the Events Themselves

There’s an even deeper layer to the problem. Prediction markets often center on decisions made in small, opaque rooms.

Interest rate moves, legislative outcomes, strategic operations—these are not phenomena that emerge from open systems. They originate from tightly held processes.

That means the informational landscape is inherently uneven. Some people are structurally closer to the truth before it becomes public.

Trying to flatten that advantage entirely would require excluding the very participants who have the most informed perspectives. But including them reintroduces asymmetry.

The system cannot be both fully inclusive and fully equal.

What This Leaves Us With

Put all of this together and a pattern emerges:

- Information asymmetry is not a bug in prediction markets. It’s part of their operating environment.

- Enforcement narrows the gap but cannot close it.

- Social networks, not just data systems, determine how information flows.

- The most accurate signals are often the least observable.

So prediction markets settle into an uneasy equilibrium. They are neither pristine truth engines nor rigged games. They are instruments shaped by competing forces that never fully cancel each other out.

A more grounded way to see them is this:

They are tools for extracting some signal from a noisy world, under conditions where perfect symmetry is impossible and perfect knowledge is unreachable.

The interesting question is not whether they can be made flawless. It’s where society decides to draw the line between informational richness and acceptable fairness, knowing that whichever direction it leans, something important is being traded away.

Leave a Reply