- ■

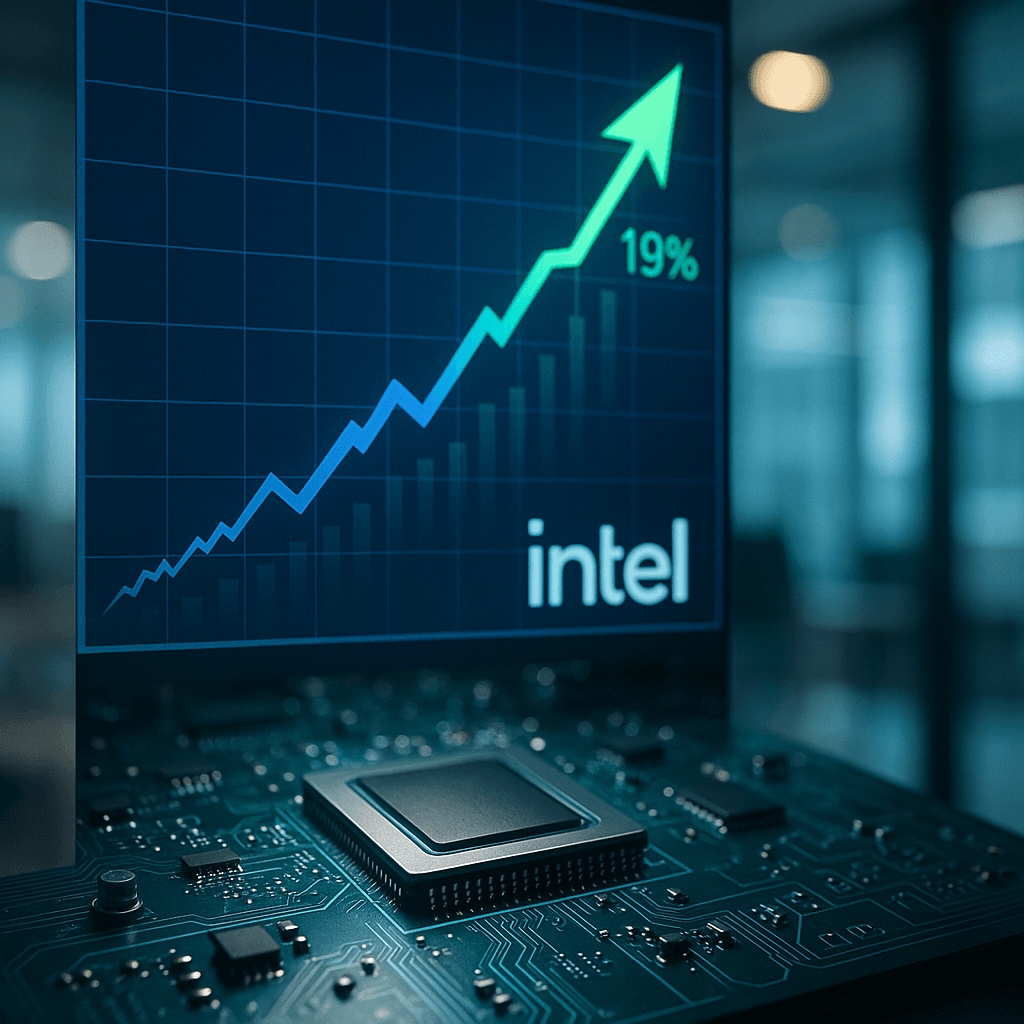

Intel’s stock soared 19% after Q1 2026 earnings topped analyst estimates, according to CNBC reporting

- ■

The earnings beat marks a potential turning point for the chipmaker’s multi-year restructuring effort

- ■

Results come as Intel battles to regain relevance against Nvidia and AMD in AI and data center chips

- ■

Wall Street had been betting on Intel’s comeback despite ongoing business challenges and market share losses

Intel just pulled off what many thought impossible. The struggling chipmaker’s stock surged 19% in after-hours trading Thursday after its Q1 2026 earnings shattered Wall Street expectations, marking the company’s strongest quarterly performance in over two years. The surprise beat signals that CEO Pat Gelsinger’s costly turnaround strategy might finally be gaining traction, even as Intel continues to lose ground to Nvidia in the red-hot AI chip market.

Intel just delivered the kind of quarter that’s been missing from its playbook for far too long. The chipmaker’s Q1 2026 results sent shares rocketing 19% higher in extended trading Thursday, a massive vote of confidence from investors who’ve watched the company struggle through one of the most brutal stretches in its 50-plus-year history.

The earnings beat comes at a critical moment. Intel has been fighting a two-front war – trying to rebuild its manufacturing prowess while simultaneously catching up in AI chips, where Nvidia has run away with the market. Wall Street had grown surprisingly optimistic about Intel’s prospects in recent months, even as the actual business showed little concrete progress. Thursday’s results suggest that optimism might not have been misplaced.

According to CNBC’s reporting, Intel has been “a Wall Street darling of late even as the business has yet to find much momentum.” That contradiction – high investor sentiment meeting lackluster fundamentals – made this quarter a make-or-break moment for the company’s credibility.

The 19% post-earnings pop represents one of Intel’s strongest single-day moves in years, putting it in rare company among mega-cap tech stocks. For context, that’s the kind of explosive reaction typically reserved for high-growth startups, not legacy semiconductor manufacturers with $50 billion-plus annual revenues. The magnitude of the move suggests Intel didn’t just beat estimates – it likely crushed them across multiple metrics.

CEO Pat Gelsinger has been on a mission since returning to Intel in 2021, pledging to restore the company’s manufacturing leadership and reclaim the performance crown from rivals like AMD. But that strategy came with a brutal price tag – tens of billions in capital expenditures for new fabs, pressure on margins, and years of delayed gratification for investors. The Q1 results might be the first real evidence that Gelsinger’s gamble is paying off.

The competitive landscape makes this quarter even more significant. While Nvidia continues to dominate AI accelerators with its H100 and newer Blackwell chips, and AMD gains ground in data center CPUs, Intel has been stuck in a holding pattern. The company’s Gaudi AI accelerators have failed to gain meaningful traction, and its core CPU business has hemorrhaged server market share. Any signs of stabilization or – better yet – growth would mark a major inflection point.

Investors had been positioning for an Intel comeback despite the challenges. The stock had climbed steadily heading into earnings, with hedge funds and retail traders alike betting that the worst was behind the company. Thursday’s results validate that thesis, at least for now. The question is whether Intel can sustain the momentum or if this represents a temporary bright spot in an otherwise difficult transition.

The timing couldn’t be more critical for Intel. The company is racing to launch its 18A manufacturing process, which Gelsinger has positioned as the technology that will finally put Intel back on equal footing with TSMC, the Taiwanese giant that manufactures chips for Apple, Nvidia, and AMD. Any revenue growth or margin improvement in Q1 likely means Intel is successfully managing the balancing act between investing for the future and delivering results today.

For the broader semiconductor industry, Intel’s strong quarter arrives amid mixed signals. Memory chipmakers have seen prices stabilize after a brutal downturn, while the AI chip boom continues to lift Nvidia and its suppliers. But traditional PC and server markets remain choppy, making Intel’s beat all the more impressive if it came from these core segments.

The market’s enthusiastic response also reflects something deeper – investors desperately want to believe in an Intel turnaround story. The company remains America’s flagship semiconductor manufacturer at a time when chip sovereignty has become a national security priority. Washington has committed billions through the CHIPS Act to support domestic production, with Intel as the primary beneficiary. A successful Intel comeback isn’t just good for shareholders – it’s central to U.S. technology strategy.

What remains unclear is which specific business units drove the outperformance. Did Intel’s data center business finally stabilize? Are PC chip sales recovering faster than expected? Or did the company’s nascent foundry business – which aims to manufacture chips for other companies – start gaining customer wins? The answers will determine whether this quarter represents a genuine turning point or just a statistical blip.

Intel’s explosive post-earnings rally delivers the kind of validation Pat Gelsinger’s turnaround strategy desperately needed. But one strong quarter doesn’t erase years of execution missteps and competitive losses. The real test comes in the quarters ahead – can Intel prove this marks an inflection point rather than a head fake? With billions in CHIPS Act funding, the 18A process node launching soon, and AI competition intensifying, the chipmaker faces its most consequential stretch in decades. Wall Street just signaled it’s willing to believe again. Now Intel has to deliver the sustained growth to match the hype.

Leave a Reply